Posted by: thepinetree on 11/28/2018 10:37 PM

Updated by: thepinetree on 11/28/2018 10:37 PM

Expires: 01/01/2023 12:00 AM

:

The Federal Reserve's Framework for Monitoring Financial Stability ~ Chairman Jerome H. Powell

New York, NY...It is a pleasure to be back at the Economic Club of New York. I will begin by briefly reviewing the outlook for the economy, and then turn to a discussion of financial stability. My main subject today will be the profound transformation since the Global Financial Crisis in the Federal Reserve's approach to monitoring and addressing financial stability. Today marks the publication of the Board of Governors' first Financial Stability Report. Earlier this month, we published our first Supervision and Regulation Report. Together, these reports contain a wealth of information on our approach to financial stability and to financial regulation more broadly. By clearly and transparently explaining our policies, we aim to strengthen the foundation of democratic legitimacy that enables the Fed to serve the needs of the American public.

Outlook and Monetary Policy

Congress assigned the Federal Reserve the job of promoting maximum employment and price stability. I am pleased to say that our economy is now close to both of those objectives. The unemployment rate is 3.7 percent, a 49-year low, and many other measures of labor market strength are at or near historic bests. Inflation is near our 2 percent target. The economy is growing at an annual rate of about 3 percent, well above most estimates of its longer-run trend.

For seven years during the crisis and its painful aftermath, the Federal Open Market Committee (FOMC) kept our policy interest rate unprecedentedly low--in fact, near zero--to support the economy as it struggled to recover. The health of the economy gradually but steadily improved, and about three years ago the FOMC judged that the interests of households and businesses, of savers and borrowers, were no longer best served by such extraordinarily low rates. We therefore began to raise our policy rate gradually toward levels that are more normal in a healthy economy. Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy‑‑that is, neither speeding up nor slowing down growth. My FOMC colleagues and I, as well as many private-sector economists, are forecasting continued solid growth, low unemployment, and inflation near 2 percent.

There is a great deal to like about this outlook. But we know that things often turn out to be quite different from even the most careful forecasts. For this reason, sound policymaking is as much about managing risks as it is about responding to the baseline forecast. Our gradual pace of raising interest rates has been an exercise in balancing risks. We know that moving too fast would risk shortening the expansion. We also know that moving too slowly--keeping interest rates too low for too long--could risk other distortions in the form of higher inflation or destabilizing financial imbalances. Our path of gradual increases has been designed to balance these two risks, both of which we must take seriously.

We also know that the economic effects of our gradual rate increases are uncertain, and may take a year or more to be fully realized. While FOMC participants' projections are based on our best assessments of the outlook, there is no preset policy path. We will be paying very close attention to what incoming economic and financial data are telling us. As always, our decisions on monetary policy will be designed to keep the economy on track in light of the changing outlook for jobs and inflation.

Under the dual mandate, jobs and inflation are the Fed's meat and potatoes. In the rest of my comments, I will focus on financial stability--a topic that has always been on the menu, but that, since the crisis, has become a more integral part of the meal.

Historical Perspective on Financial Stability

The term "financial stability" has a particular meaning in this context. A stable financial system is one that continues to function effectively even in severely adverse conditions. A stable system meets the borrowing and investment needs of households and businesses despite economic turbulence. An unstable system, in contrast, may amplify turbulence and prolong economic hardship in the face of stress by failing to provide these essential services when they are needed most.

For Economic Club of New York trivia buffs, I will note that the second ever presentation to this club by a Federal Reserve official was about this very topic. The date was March 18, 1929. Weeks before, the Fed had issued a public statement of concern over stock market speculation, and had provided guidance frowning on bank funding of such speculation. William Harding, a former Fed Chair and then president of the Federal Reserve Bank of Boston, defended the Fed's actions in his talk. He argued that, while the Fed should not act as the arbiter of correct asset prices, it did have a primary responsibility to protect the banking system's capacity to meet the credit needs of households and businesses. At the meeting, critics argued that public statements about inflated asset prices were "fraught with danger;" that the nation's banks were so well managed that they should not "face public admonition"; and, more generally, that the Fed was "out of its sphere."1 Of course, Harding spoke just a few months before the 1929 stock market crash, which signaled the onset of the Great Depression.2

Fast forwarding, a host of Depression-era reforms helped avoid, for the next three-quarters of a century, a systemic financial crisis and the associated severe economic dislocation‑‑the longest such period in American history. Those decades saw many advances in monetary policy and in bank regulatory policy, but the appropriate role for government in managing threats to the broader financial system remained unresolved. Periodic bouts of financial stress during this period--such as the Latin American debt crisis, the savings and loan crisis, and the Russian debt default--were met with improvised responses. Policymakers conjured fixes from a mixture of private-sector rescues, emergency liquidity, occasional implicit or explicit bailouts, and monetary accommodation. Outside of these crisis responses, however, systemic issues were not a central focus of policy.

The Global Financial Crisis demonstrated, in the clearest way, the limits of this approach. Highly inventive and courageous improvisation amid scenes of great drama helped avoid another Great Depression, but failed to prevent the most severe recession in 75 years. The crisis made clear that there can be no macroeconomic stability without financial stability, and that systemic stability risks often take root and blossom in good times.3 Thus, as the emergency phase of the crisis subsided, Congress, the Fed, and the other financial regulators began developing a fundamentally different approach to financial stability. Instead of relying on improvised responses after crises strike, policymakers now constantly monitor vulnerabilities and require firms to plan in advance for financial distress, in a framework that lays out solutions in advance during good times.

The New Approach to Financial Stability

This new approach can be divided into three parts. First, build up the strength and resilience of the financial system. Second, develop and apply a broad framework for monitoring financial stability on an ongoing basis. And third, explain the new approach as transparently as possible, so that the public and its representatives in Congress can provide oversight and hold us accountable for this work. Although I'll focus mainly on the stability efforts of the Federal Reserve, a number of federal regulatory agencies have responsibilities in this area. All of these agencies are represented on the Financial Stability Oversight Council, or FSOC, which is chaired by the Treasury Secretary and which provides a forum for interagency cooperation in responding to emerging risks.

Building Resilience of the Financial System

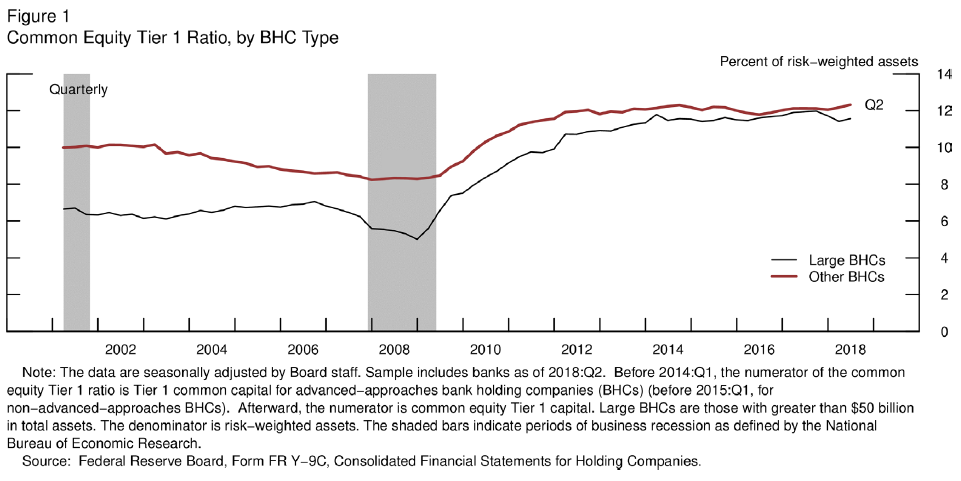

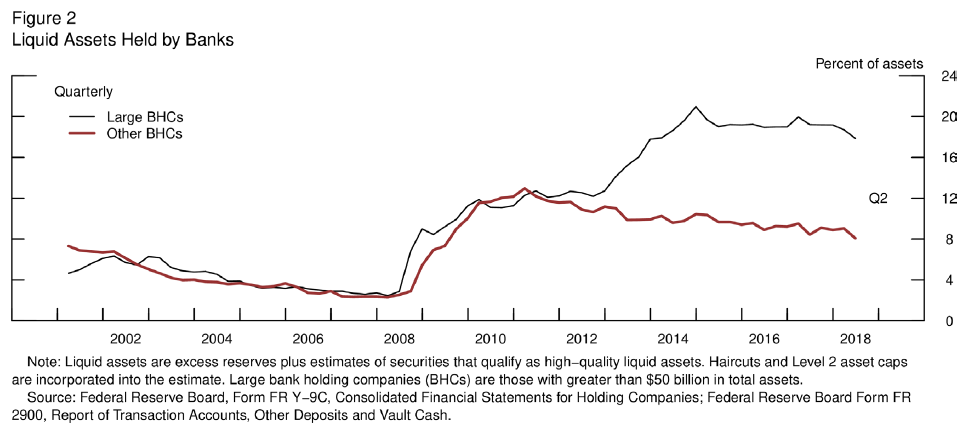

After 10 years of concentrated effort in the public and private sectors, the system is now much stronger, with greater capacity to function effectively in stressful times. In the banking system, we have implemented a post-crisis regulatory framework based on robust capital and liquidity requirements, a strong stress-testing regime, and mandatory living wills for the largest firms. As a result, banks now have much more high quality capital than before (figure 1). The most recent stress tests indicate that, even after a severe global recession, capital levels at the largest banks would remain above regulatory minimums, and above the levels those banks held in good times before the crisis.4 The most systemically important financial institutions also now hold roughly 20 percent of their assets in the form of high quality liquid assets--that is, safe assets that could be readily sold at short notice (figure 2). The share of these assets is about four times its pre-crisis level.

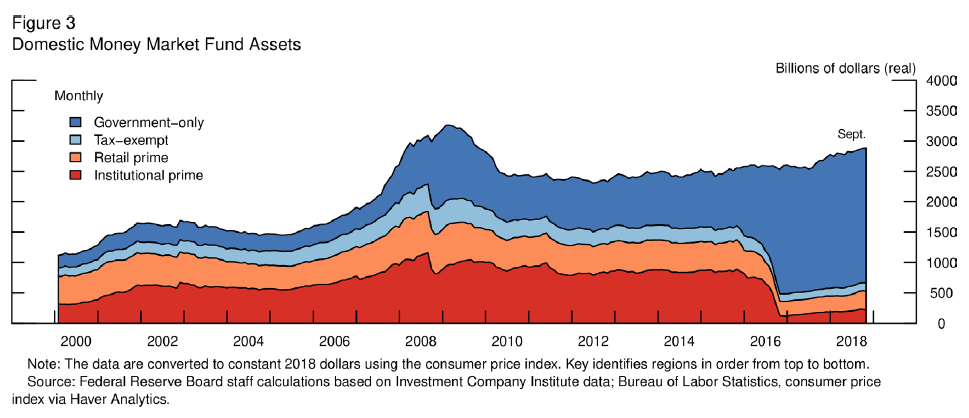

Compared with other economies, lending and borrowing in the United States depend less on bank loans and more on funds flowing through a wide array of capital market channels. The crisis revealed that this capital market centric system, despite its many benefits, also provides more places where systemic risks can emerge. In response, Congress and the regulatory agencies have made many stability-enhancing changes outside of the banking system. For example, many derivatives transactions are now required to be centrally cleared, which, through netting, has reduced exposures and enabled better management of counterparty risk. Tri-party repurchase agreement (repo) reforms have substantially improved the resilience of that marketplace, in particular by limiting intraday loans. Before the crisis, prime institutional money market funds were permitted to report a constant, $1 share price so long as the value of the underlying assets remained near $1. This reporting convention, combined with the implicit support of the plans' sponsors, led investors to treat those funds like bank deposits, even though they were not likewise insured. These funds are now required to report floating net-asset values, and after this reform investors chose to migrate to government-only funds, which are safer and less susceptible to runs (figure 3).5 These and other measures have reduced the risk that key non-bank parts of the system would freeze up in the face of market stress.

A New Framework for Monitoring Systemic Risks

Innovation and risk-taking contribute to the dynamism of our financial system and our economy. As Hyman Minsky emphasized, along with the many benefits of dynamism comes the reality that the financial system will sometimes evolve toward excess and dangerous imbalances.6 This reality underscores the vital importance of the second part of post-crisis reform: monitoring for emerging vulnerabilities.

As laid out in our new Financial Stability Report, we have developed a framework to help us monitor risks to stability in our complex and rapidly evolving financial system. The framework distinguishes between shocks, that is, trigger events that can be hard to predict or influence, and vulnerabilities, defined as features of the financial system that amplify shocks. The report is organized around four broad vulnerabilities that have been prominent in financial crises through the centuries. Each of these vulnerabilities is often found to some degree even in healthy market-based systems, and there is not, at present, any generally accepted standard for assessing at what level the vulnerabilities begin to pose serious stability risks. In lieu of such a standard, we flag cases in which the vulnerabilities rise well beyond historical norms, and then form judgments about the stability risks those cases present.

The first vulnerability is excessive leverage in the financial sector.7 If a highly leveraged segment of the financial system is buffeted by adverse events, the affected entities may all need to deleverage at the same time by selling assets, leading to what is called a "fire sale." Both the resulting decline in asset prices and the impaired ability of the segment to play its role in the economy can amplify the effects of a downturn. We saw this chain of events play out repeatedly in various parts of the financial sector in the weeks following the failure of Lehman Brothers in 2008.

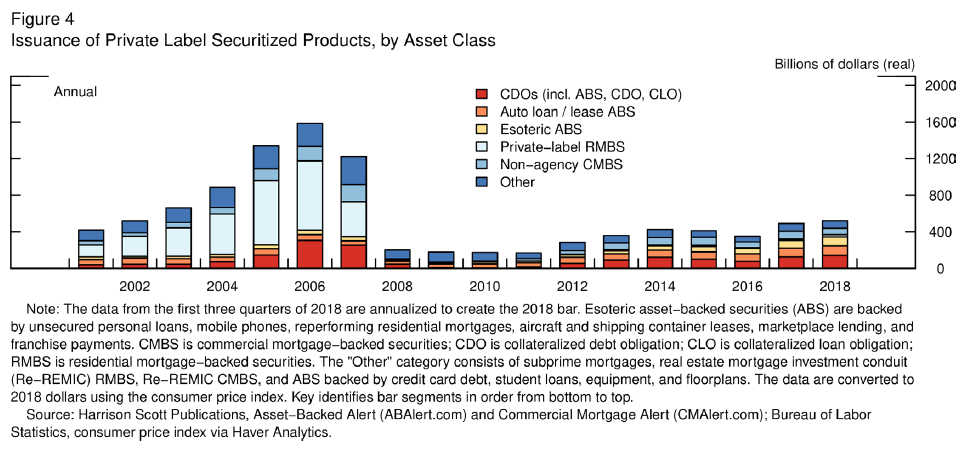

In our surveillance, we examine leverage across many types of financial institutions, including banks, insurance companies, hedge funds, and various funding vehicles. Currently, we do not detect a broad-based buildup of abnormal or excessive leverage. As with banks, capital levels at insurance companies and broker-dealers appear robust. In addition, securitization levels are far below their pre-crisis levels, and those structures that do exist rely on more stable funding (see figure 4). Our view into leverage and risk-taking outside the banking sector is admittedly incomplete, however, and we are always working to get a better view of emerging leverage excesses.8

The second vulnerability is funding risk, which arises when banks or nonbank financial entities rely on funding that can be rapidly withdrawn. If depositors or market participants lose faith in the soundness of an institution or the system as a whole, unstable funding can simply vanish in what is called a "run." During the crisis, we saw widespread runs, including at broker-dealers, some segments of the repo market, and money market mutual funds. These runs did severe damage, contributing to a generalized panic at the time. Had the authorities not stepped in, the damage could have been even more severe.

Today we view funding-risk vulnerabilities as low. Banks hold low levels of liabilities that are able and likely to run, and they hold high levels of liquid assets to fund any outflows that do occur. Money market mutual fund reforms have greatly reduced the run risk in that sector. More generally, it is short-term, uninsured funding that would be most likely to run in a future stress event, and the volume of such funding is now significantly below pre-crisis peaks.

Taken together, the evidence on these first two vulnerabilities strongly supports the view that financial institutions and markets are substantially more resilient than they were before the crisis. Indeed, the American financial system has successfully weathered some periods of significant stress over the past several years.9

The third vulnerability is excessive debt loads at households and businesses. Credit booms have often led to credit busts and sometimes to painful economic downturns. When the bust comes, those who have overborrowed tend to sharply reduce their spending. Defaults typically rise faster than had been expected, which may put financial institutions into distress. These effects may combine to bring a serious economic downturn.

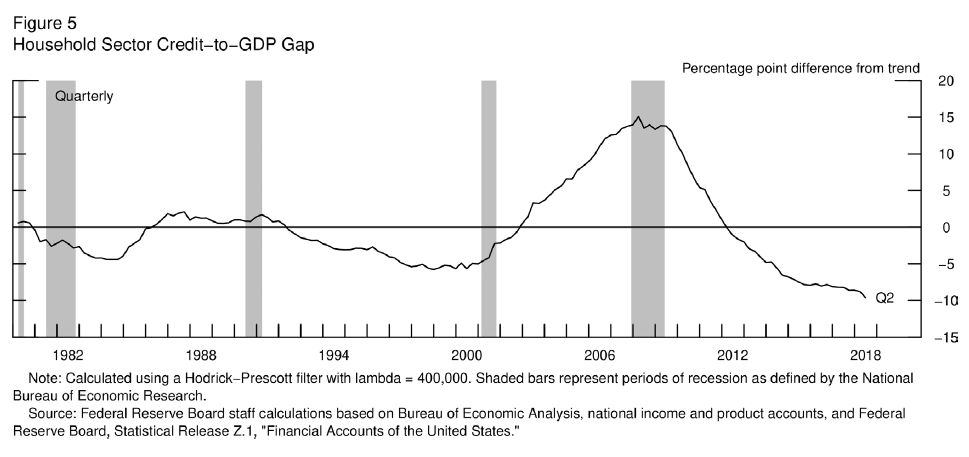

This boom-bust pattern was clear in measures of household debt around the crisis period, with mortgage debt rising far above its historical trend and then contracting sharply (see figure 5). After the contraction, household debt has grown only moderately. The net increase in mortgage debt has been among borrowers with higher credit scores. While heavily indebted households always suffer in a downturn, all of this suggests that household debt would not present a systemic stability threat if the economy sours.

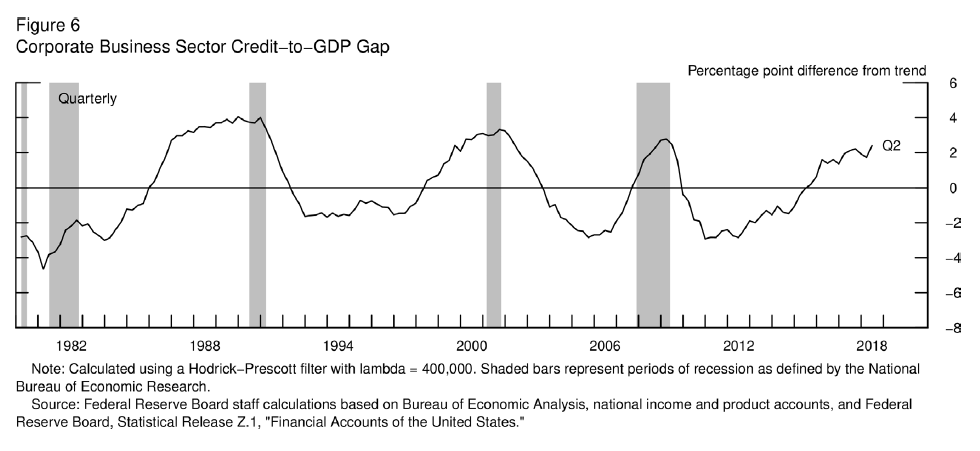

Nonfinancial business borrowing presents a subtler story. With corporate debt, the United States has not faced a massive credit boom like that experienced with residential mortgages before the recent crisis. Instead, after controlling for its trend, business borrowing relative GDP has risen during expansions, no doubt reflecting business optimism, and then fallen when the cycle turned, as some of that optimism proved unfounded (see figure 6). By this measure, the ratio of corporate debt to GDP is about where one might expect after nearly a decade of economic expansion: it is well above its trend, but not yet at the peaks hit in the late 1980s or late 1990s. Further, the upward trend in recent years appears broadly consistent with the growth in business assets relative to GDP.

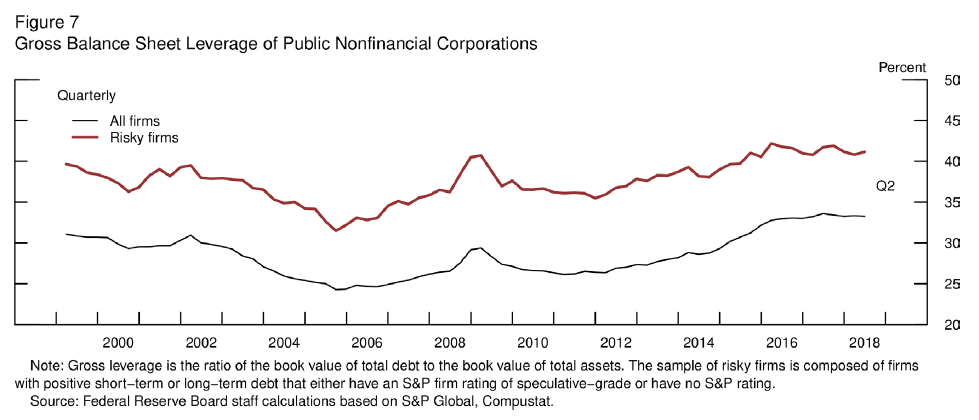

There are reasons for concern, however. Information on individual firms reveals that, over the past year, firms with high leverage and interest burdens have been increasing their debt loads the most (see figure 7). In addition, other measures of underwriting quality have deteriorated, and leverage multiples have moved up. Some of these highly leveraged borrowers would surely face distress if the economy turned down, leading investors to take higher-than-expected losses--developments that could exacerbate the downturn. The question for financial stability is whether elevated business bankruptcies and outsized losses would risk undermining the ability of the financial system to perform its critical functions on behalf of households and businesses. For now, my view is that such losses are unlikely to pose a threat to the safety and soundness of the institutions at the core of the system and, instead, are likely to fall on investors in vehicles like collateralized loan obligations with stable funding that present little threat of damaging fire sales.10Of course, we will continue to monitor developments in this sector carefully.

The fourth and final vulnerability arises when asset values rise far above conventional, historically observed valuation benchmarks--a phenomenon popularly referred to as a "bubble." The contentious term "bubble" does not appear in our work, however.11 Instead, we focus is on the extent to which an asset's price is high or low relative to conventional benchmarks based on expected payoffs and current economic conditions. Historically, when asset prices soar far above standard benchmarks, sharp declines follow with some regularity, and those declines may bring economic misery reaching far beyond investors directly involved in the speculative boom. We therefore pay close attention when valuations get to the extreme ends of what we have seen in history.

Looking across the landscape of major asset classes, we see some classes for which valuations seem high relative to history. For example, even after standard adjustments for economic conditions, valuations on riskier forms of corporate debt and commercial properties are in the upper ends of their post-crisis distributions, although they are short of the levels they hit in the pre-crisis credit boom. We see no major asset class, however, where valuations appear far in excess of standard benchmarks as some did, for example, in the late 1990s dot-com boom or the pre-crisis credit boom.

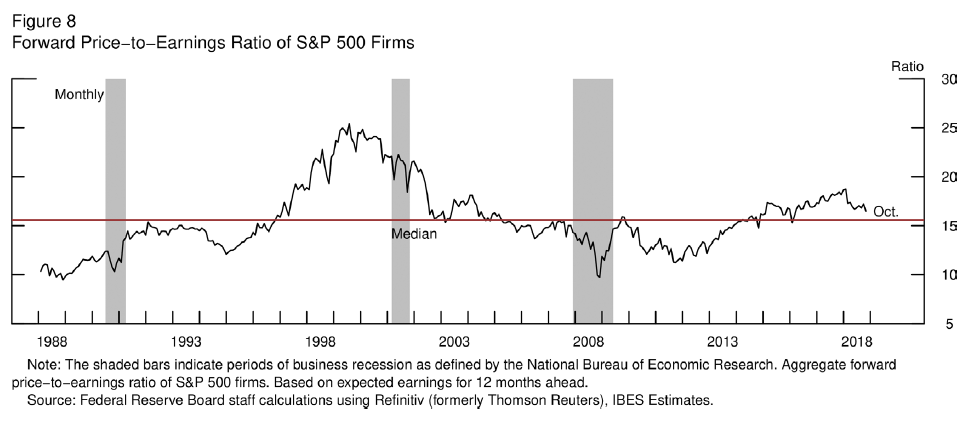

The asset class that gets the most attention day-to-day is, of course, the stock market. Today, equity market prices are broadly consistent with historical benchmarks such as forward price-to-earnings ratios (see figure 8). It is important to distinguish between market volatility and events that threaten financial stability. Large, sustained declines in equity prices can put downward pressure on spending and confidence. From the financial stability perspective, however, today we do not see dangerous excesses in the stock market.

Monitoring Likely Triggers for Financial Distress

I mentioned the distinction between vulnerabilities and shocks, or triggers. In addition to monitoring vulnerabilities under our four-part framework, we also consult a broad range of contacts regarding sources of risk that might trigger distress at any given time. For example, discussions with contacts currently point to risks emanating from the normalization of monetary policy in the United States and elsewhere, the unsettled state of trade negotiations, Brexit negotiations, budget discussions between Italy and the European Union, and cyber-related disruptions.12

Having identified possible triggers, we can assess how a particular trigger is likely to interact with known vulnerabilities. A good current example is that of Brexit. U.S. banks and broker-dealers participate in some of the markets most likely to be affected by Brexit. The Fed and other regulators have been working with U.S. financial institutions that have operations in the European Union or the United Kingdom to prepare for the full range of possible outcomes to the negotiations. In addition, the scenarios used in the stress tests routinely feature severe global contractions and show that U.S. banks have the capital to weather even highly disruptive events.

Bottom Line: Financial Stability Risks Are Moderate

I have reviewed a few of the key facts that inform our thinking about financial stability, and you will find a great deal more detail in our new report. You will also find that the report does not come to a bottom line conclusion. As I noted earlier, we have limited experience with this monitoring, and there is no widely accepted basis for reaching a bottom line. Thus, the purpose of the report is to provide a common platform and set of readings from which policymakers and other interested parties can form their own views. Individual policymakers will sometimes differ in their assessments and on the relative weight they put on particular vulnerabilities. My own assessment is that, while risks are above normal in some areas and below normal in others, overall financial stability vulnerabilities are at a moderate level.13

In my view, the most important feature of the stability landscape is the strength of the financial system. The risks of destabilizing runs are far lower than in the past. The institutions at the heart of the financial system are more resilient. The stress tests routinely feature extremely severe downturns in business credit, and the largest banks have the capital and liquidity to continue to function under such circumstances. Because this core resilience is so important, we are committed to preserving and strengthening the key improvements since the crisis, particularly those in capital, liquidity, stress testing, and resolution.

Conclusion

I'd like to conclude by putting financial stability and our two new reports in a longer-term context. To paraphrase a famous line, "eternal vigilance is the price of financial stability." We will publish these reports regularly as part of our vigilance.

Over time, some may be tempted to dismiss the reports entirely or to overdramatize any concerns they raise. Instead, these reports should be viewed as you might view the results of a regular health checkup. We all hope for a report that is not very exciting. Many baby boomers like me are, however, reaching an age where a good report is, "Well, there are a number of things we should keep an eye on, but all things considered you are in good health." That is how I view the Financial Stability Report out today.

We hope that this report and the Supervision and Regulation Report will be important tools, sharing Federal Reserve views and stimulating public dialogue regarding the stability of the financial system.

1. See remarks of W.P.G. Harding at a dinner of the Economic Club of New York on March 18, 1929, as reported in "Clash on Policies of Reserve Board" by the New York Times on March 19, 1929, p. 52; and in "Reserve Policy Upheld and Hit" by the Wall Street Journal on March 19, 1929, p. 21. Also see "Wall Street News and Comment," Special Dispatch to the [Daily Boston] Globe, on March 24, 1929, p. A60. Return to text

2. Many factors after the initial crash, including what are now seen as major policy errors, contributed to the Great Depression. See Milton Friedman and Anna Jacobson Schwartz (1963), A Monetary History of the United States, 1867-1960 (Princeton, N.J.: Princeton University Press); and Ben S. Bernanke (1983), "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression," American Economic Review, vol. 73 (June), pp. 257-76. Return to text

3. Hyman Minsky had long emphasized this point. For instance, see Hyman P. Minsky (1991), "Financial Crises: Systemic or Idiosyncratic (PDF)," Working Paper 51, prepared for presentation at "Crisis in Finance," a conference of the Jerome Levy Economics Institute, Bard College, April. Return to text

4. See the Federal Reserve's November 2018 Supervision and Regulation Report, available on the Board's website. Return to text

5. Given that government money fund asset holdings are limited to safe assets, they are allowed to maintain a $1 share price. Return to text

6. See Minsky, "Financial Crises," in note 3. Return to text

7. A more highly leveraged sector is one that relies more heavily on borrowed money. Return to text

8. Sometimes we look to bank lending for information. Data from the stress tests suggest that the nation's largest banks have committed about $1 trillion in lines of credit to nonbanks. Return to text

9. Examples include episodes of intensified concerns over euro-area fiscal challenges, the discontinuous and large appreciation of the Swiss franc in January 2015, and the market volatility associated with global growth concerns in late 2015. Return to text

11. Analysts differ over how to define the term "bubble," and debate continues about the degree to which economic fundamentals might explain even the most famous apparent bubble cases from history. On the topic of tulip mania, for example, see Peter M. Garber (1989), "Tulipmania," Journal of Political Economy, vol. 97 (June), pp. 535-60." Return to text

12. The Financial Stability Report does not currently have a standard set of metrics for determining the resiliency of critical financial systems to cyber disruptions. Nonetheless, cyber risks are the subject of ongoing policy efforts at that Federal Reserve and other relevant agencies, and these entities are working to develop resiliency expectations and measures, which may be part of future discussions in the stability report. Return to text

13. The staff have also assessed financial stability vulnerabilities as moderate. For instance, see the minutes of the Federal Open Market Committee meeting, July 31-August 1, 2018, available on the Board's website. Return to text

The comments are owned by the poster. We are not responsible for its content. We value free speech but remember this is a public forum and we hope that people would use common sense and decency. If you see an offensive comment please email us at news@thepinetree.net

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}