Posted by: thepinetree on 03/28/2011 11:50 AM

Updated by: Kim_Hamilton on 03/28/2011 07:33 PM

Expires: 01/01/2016 12:00 AM

:

The FEMA Scheme ~ By David Tunno

Valley Springs, CA...At the request of Rancho Calaveras residents Bob and Char Stanton in early January of 2011, I was asked to look into the actions by the Federal Emergency Management Agency (FEMA) in preparation for a meeting with FEMA representative Kathleen Schaefer and others on January 26th at the County offices and to represent the Stanton’s in that meeting. My investigation of the facts surrounding the Stantons’ example and others in the County revealed what appears to be a massive fraud on the part of FEMA, not just on Calaveras residents, but on potentially millions across the U.S...

whose properties have been recently placed by FEMA in a flood zone, triggering numerous and costly consequences for those property owners.

The evidence will show that the chance of a flood, even in a 100 years (the standard for flood zone designations), occurring on the Stanton’s property, and those of their neighbors likewise affected, is as close to zero as can be imagined. The question then becomes, how did those properties acquire flood status from FEMA?

The question of “how” quickly changed to a new starting point, “why?” The answer, which goes to FEMA’s motives, was revealed in that 1/26/11 meeting.

To begin with, it must be understood that, for many years, flood insurance has not been available in the private insurance market. All flood insurance coverage is underwritten by the federal government via the National Flood Insurance Program (NFIP), a division of FEMA.

In attendance on 1/26/11 were; Ms. Schaefer, Robert Elhert of Congressman Dan Lundgren’s office, David Pastizzo of the County’s Planning Department, District Five Supervisor Darren Spellman, the Stanton’s and me.

By way of providing foundation for FEMA’s new flood maps, Ms. Schaefer revealed, possibly inadvertently, FEMA’s motive. Massive and destructive flooding in the hurricane belt (including Katrina) and the drainage areas of the Mississippi, its tributaries and other flood-prone regions in past years has hit FEMA hard. Any reserves it had were wiped out and taxpayers have had to foot the bill for those disasters.

Following up that information with a brief online research effort turned up evidence consistent with that disclosure and expanding on it. One helpful site posted a tutorial slide show that provided a history of how we got to where we are. It was neutral and did not appear to take a position on FEMA.

It showed that the NFIP was formed in 1968. The objective was to create a flood insurance pool that would fund flood disasters previously financed by the taxpayers. Not a bad idea, but there were unintended consequences to some of NFIP’s actions. One of those was to offer low-cost flood insurance in high-risk areas. The results were predictable as shown in the following three slides from that site:

Completing the motive picture for FEMA is a simple matter. As would be the case with any insurance underwriter, FEMA had only two choices; 1) begin charging owners of flood-prone properties a great deal more (the real costs) to cover the risks, or 2) spread the risk over a greater number of policy holders.

Choice #1 would likely have led to astronomical prices for policies and would have, therefore, politically untenable. Choice #2, on the other hand, carried with it one very important requirement. Adding more policy holders in actual flood zones would not solve FEMA’s problem. The new policy holders must represent virtually no risk of a payout.

FEMA chose plan #2, and in doing so cast a net over potentially millions of American property holders who, like the Stanton’s, represent no risk of exposure. In this way, FEMA could build its reserves for the next disaster event, paid for by those millions of new policy holders who don’t need a policy and to whom it will never have to pay out a dime in coverage. All those new premiums represent free money, subsidies for property owners in high-risk areas and a prime example of taxation through regulation on a massive scale. FEMA has used two tools in achieving its goal – the proverbial carrot and stick.

Every day one sees on television an ad for flood insurance. A man, speaking as though he is a house, stands under a suspended portion of roof and tries to convince others doing likewise to get flood insurance. In the corner of the screen is a website, floodsmart.gov. Floodsmart.gov is the FEMA/NFIP site. Googling “FEMA flood map” will produce that site at the top of the page where websites pay for top exposure and where they can include messages to drive traffic to their sites. FEMA’s message, as shown below, is quite extraordinary:

1. Flood Information & Facts

Everyone is at Risk - Find Out How to Protect Your Home & Your Family!

www.floodsmart.gov

“Everyone is at Risk,” really? Not just people in flood-prone areas, but “everyone?” As it turns out, that’s one of the “carrots,” encouraging (a generous interpretation) people to voluntarily buy flood insurance. The “stick” is something else again. It forces property owners to buy insurance.

Each of the property owners affected in Calaveras County was to have been sent a notice by the County, which also included notices of public meetings featuring Ms. Schaefer of FEMA. The Stantons attended one of those meeting on October 26 of 2010.

At that meeting, Ms. Schaefer told those gathered that “best engineering practices” were used to identify those properties that were added to the flood map. The map is available on the County’s website. To get the full impact, one must zoom in and scroll around to see all the red lines that represent new flood zones FEMA has added to the county map.

The above portion is a close-up view of the area that includes the Stanton property in Rancho Calaveras. There are red lines everywhere, and they are all new.

One piece of information the Stanton’s did not hear at that meeting was the answer to the question, “For a property owner whose house is nowhere near a source of flooding, what can be done about this?” The Stantons had to find out from their own research that the answer is to get a Letter of Map Amendment (LOMA). The bottom line is this, if FEMA has put any part of your property in a flood zone, no matter how far the predicted water problem is from your house, it is up to the property owner to prove the flood zone doesn’t include the house. Your property is guilty until proven innocent. That’s where the LOMA comes in.

The Stanton’s research also revealed that there was a do-it-yourself LOMA application procedure that was only available until Dec. 31, 2010, a scant few weeks following the public meetings. After that date, a LOMA requires the services of certified engineer or surveyor at a cost of up to $2,000. Indeed, a cottage industry has sprung up to sell engineering services to property owners who need a LOMA but missed the do-it-yourself deadline.

Notwithstanding the LOMA procedure, the Stanton’s, and everyone who received notice that their property was now in a flood zone, were “encouraged” to buy flood insurance and, again, FEMA used a carrot-and-stick approach.

The “carrot” was an insurance policy with a relatively low price for a limited period - a sort of “Buy-It-Now” price. In the Stanton’s case the buy-it-now price was $495 a year. That price was to be good until December 17, 2010, just a couple months after the public meeting. For those who missed that deadline, they were told the price would be $2,000 (A.K.A. the “stick”). The $495 price itself was to be good for only three years. After that, there was no indication of what the rate would be.

According to the Stantons, Ms. Schaefer admitted that FEMA’s flood map was a work in progress, but warned those present that if they didn’t get insurance now, they could be hit with the higher premiums later.

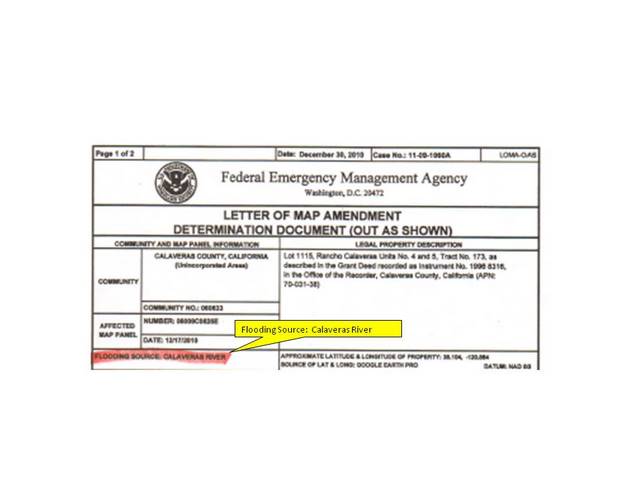

Some, who undoubtedly did not want to gamble, took the bait and bought the insurance. Mission accomplished for FEMA. Others, like the Stanton’s, did their homework and got their LOMA. That two-page document now shows their house is not in the flood zone, but it goes a bit farther and, in doing so, reveals the quality of FEMA’s “best engineering practices” that went into their flood zone designation in the first place.

The Stantons’ LOMA revealed FEMA’s reasoning regarding their property and prompted them to prove the property never should have been included.

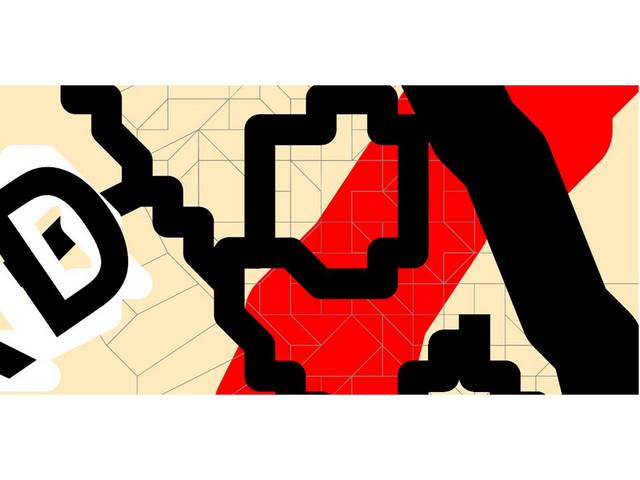

The portion of the Stantons’ LOMA shown above includes what FEMA considered to be the source of flooding on their property, the Calaveras River. For that 1/26/11 meeting, Bob Stanton, using a topographical map of the area showing elevations, drew the diagram below.

It shows their property (marked with an “X”) in relationship to the Calaveras River. The diagram shows the Stanton’s property is about 40 feet below the crest of a hill that separates it from the river. For all practical purposes, as relates to the Stanton’s property, the hill represents a continuous barrier to the river. It shows that in order for the Calaveras River to be the source of flooding on their property the depth of the river would have to rise over 240 feet. This is a portion of the river downstream from the New Hogan dam, built to prevent floods.

It should be noted that from the Stanton’s property, let alone the top of the hill a bit further up the street, one can see all the way across the San Joaquin valley to Mt. Diablo. The mountain can be seen almost to the San Joaquin Valley floor nearly 70 miles away. It should also be understood that there are no land masses between their property and the valley that would halt the flow of water. The water has a relatively clear path down the hill and it is a relatively steep downhill run all the way to the eastern edge of the valley.

One needn’t be an engineer to know that water seeks its own level and runs downhill. So, in order for the Stanton’s property to be flooded by the Calaveras River, the San Joaquin valley would also have to be under water by a few hundred feet, which, in turn, would require a massive land mass to move into place preventing the water from flowing into the San Francisco Bay and out to sea. After considerable prodding, Ms. Schaefer admitted that the source of flooding in the Stanton’s LOMA could not be the Calaveras River.

Given the evidence above, that admission came as no surprise. Despite the verbal claim of “best engineering practices,” the LOMA itself includes the following language on page two:

The National Flood Insurance Program map affecting this property depicts a Special Flood Hazard Area that was determined using the best flood hazard data available to FEMA, but without performing a detailed engineering analysis. The flood elevation used to make this determination is based on approximate methods and has not been formalized through the standard process for establishing base flood elevations published in the Flood Insurance Study. This flood elevation is subject to change.

That language is stark contrast and directly contradicts a claim of “best engineering practices.” Nevertheless, the Stanton’s had to prove FEMA’s information was incorrect and everyone who also received their notice was pushed to get flood insurance.

Having been shown the Calaveras River could not be a source of flooding on their property, or any of the properties similarly situated, FEMA resorted to a new rationale. The source of flooding was now the drainage gully itself, that is, the slopes of the watershed along which the Stantons’ home was built, are predicted by FEMA, in a 100-year period, to produce enough water from rainfall to flood the gully. This is not a basin, but a gully that is completely open on the west end, the end toward the San Joaquin Valley.

The above satellite image shows the Stanton’s property and the neighboring properties with a large blue zone, drawn by FEMA, depicting the expected water level it predicts would be realized in such a flood event. Using this graphic, Bob Stanton identified a tree on his property that marks the upper limit of FEMA’s flood outline. By his measurement, the water at that point would be approximately 12 feet deep. Google Earth shows that point at about 430 feet above sea level.

Bob also took photos of the gully on and near the Stanton’s property on December 19-22, 2010 during what The Weather Channel reported was a “Pineapple Express” storm – record-breaking rains - the worst in a decade.

The photos show a shallow stream of water resulting from that record storm. That is all the slopes produced.

The first photo shows a four-foot diameter culvert that runs under Baldwin Street about a quarter mile down slope from the Stantons’ property. Baldwin, at that point is 355 feet above sea level (source: Google Earth). The entire drainage gully picks up after Baldwin and continues down slope to a relatively flat zone in the Jenny Lind area, not quite a mile away and about 240 feet below the elevation of the Stanton’s property. That is the “clear path” mentioned earlier – steeply sloping land with no barriers to the flow of water all the way to the eastern edge of the San Joaquin Valley floor.

As before, in order for the Stanton’s property to see the water level depicted in the satellite photo/graphic, Baldwin Street itself would have to be 75 feet under water, which means homes down slope from the Stantons’ would be under water well over their roof tops. Indeed, homes down slope, even if they were nowhere near a creek or drainage ditch of any kind, and which are currently not designated by FEMA to be in a flood zone, would be deep under water, as would the San Joaquin Valley.

Conceptually, the graphic below (not to scale) depicts a cross-sectional view of the results of FEMA’s engineering regarding the Stantons’ property flood status. The photo in the graphic that follows it was taken at Baldwin Street. The graphic representation is also not to scale.

Clearly, no FEMA representative ever set foot on the Stantons’ property prior to placing it in a flood zone, for even a casual drive by would have proven to anyone, competent engineer or not, the falsity of that designation.

Looking back at the same map graphic shown earlier, and with apologies for the low resolution, the source of water on the Stantons’ property was shown as a “river.” The water flow, shown at its zenith in 2010 in a previous set of photos was labeled “river.” Protesting that designation, Bob Stanton visited the Planning Department offices once or twice a week for over two months before the department agreed to change the designation to “seasonal drainage.”

That is some seasonal drainage; nevertheless, it is consistent with the phrase used by Kathleen Schaefer of FEMA in answer to the repeated question by Bob Stanton, “Where is the water coming from?” Her answer? “Runoff.”

The ability of the County Planning Department to change designations on a FEMA map raises a question. To what extent is the department, with its local knowledge; providing objective oversight to FEMA’s work; partnering with FEMA to advance FEMA’s agenda; or to what extent does it simply find itself forced to cooperate with FEMA? More on that later, but first another example of a FEMA flood zone parcel.

The Copperopolis home above belongs to the Farnsworths, Nick and Renee. It is situated on a loop of road with houses on both sides, as shown in the FEMA flood maps below.

According to FEMA, a flood zone cuts through the neighborhood, but there are no drainage ditches, gullies or creeks associated with that red flood zone designation, which, again, even a drive by look see would have confirmed.

Nick and Renee claim not to have received notification from the County as to their new flood status, but did get a notice from their bank, Wells Fargo, requiring them to purchase flood insurance. Their efforts led them to a FEMA contact in Colorado, Mr. Tom Birney, who punched up their parcel on his computer. The conversation with Mr. Birney, according to the Farnsworths, concluded with him telling them that FEMA had apparently used an older topographical map of the area, showing a stream bed flowing through that area (long before the neighborhood existed), and an admission that something may be wrong with FEMA’s conclusions.

In a follow-up call to Mr. Birney, he informed me that he is not a FEMA employee, but works for Michael Baker Engineering, a contractor for FEMA. His company, along with two others nationwide, is hired to rule on the LOMA applications. In this rare instance, however, and at the request of the Calaveras County Planning Department, his company would be looking into the Farnsworth’s situation, a message he had previously relayed to the Farnsworths. That has given them some hope that they will not have to spend thousands of dollars to correct FEMA’s flood map, not just for themselves, but for their entire neighborhood. In the meantime, Wells Fargo is requiring them to get insurance and won’t halt that process without say so from FEMA.

The use by FEMA of a private contractor in that role raises yet more issues and questions. How is it that a private contractor has the power to rule on the flood zone status of a property, and therefore any government regulations (including mandatory insurance) that inure from that ruling, not to mention the de-valuing of that property, and all from many hundreds of miles away, without ever setting foot thereon? Further, what incentive, if any, does that contractor have in making rulings that run contrary to the financial interests of its employer, FEMA?

Returning to the Stantons’ “runoff” problem, an apparent inconsistency surfaces regarding FEMA’s flood designations.

The photo above was taken on March 12, 2010 along the east side of Highway 26 in Rancho Calaveras. It is the drainage ditch right next to the road. It had rained recently, but not heavily and the water in the above photo is about six inches deep.

The photo above was taken on the same day. It is the culvert running under Baldwin Street, near the Stantons’ residence shown previously. The water was about four inches deep, but the watershed that drains to the ditch along Highway 26 is magnitudes greater than the slopes of the gully where the Stantons live. Consequently, one could assume the potential for water in the road-side ditch is greater than in the Stantons’ “seasonal drainage” gully. That said, neither the property shown on Highway 26 photo above, nor any properties along that east side of the highway in Rancho Calaveras are FEMA’s flood zone. Indeed, I cannot find anywhere on FEMA’s Calaveras County flood map where roadside drainage ditches like the one above caused the property to be placed in a flood zone.

There must be hundreds of miles of such examples, perhaps many of them with far greater drainage surfaces than the above example. As potential flood zone properties, that would affect many hundreds more properties in Calaveras County.

If FEMA’s definition of flood (revealed later) is followed to the letter, and if one would apply the same science/engineering as was used to include the Stantons’ property, why haven’t those additional properties been added to the flood map? I can only envision two possible answers. They are as follows:

1. There was no science/engineering that caused the Stantons’ property (or the Farnsworths’ for that matter) to be placed in a flood hazard area.

2. If, after the discussion of the Stantons’ property above, one can still believe it was the result of valid science and engineering, then FEMA has applied its flood criteria selectively.

If #1 is true, it would follow that all the engineering that resulted in FEMA’s flood map was at best suspect and at worst non-existent and therefore the map should be thrown out.

If #2 is true, why would they do that? That question produces only one answer in my mind. It is purely speculative and one can take it for what it is worth, but I offer the following explanation.

FEMA seems to have acted like a taxpayer who, in filling out his tax forms, pushes the envelope of deductions as far as he believes he can get away with - that is without sending up a red flag triggering an audit.

In FEMA’s case, it hasn’t altogether worked. Some cities and counties across America are pushing back. But, if FEMA had applied its flood definition and used the same engineering that affected the Stantons’ property across the board, many more properties would be included - properties whose new flood status would be known to be ridiculously false to even the casual observer. Red flags would have popped up all over America. The cooperation FEMA needs from county planning departments would have been endangered. Even the more liberal Congress of pre-2010 elections might have been compelled to “audit” FEMA.

The engineering and assumptions made regarding the Stantons’ property are examples of the quality of information use by FEMA to encourage property owners to buy insurance; however, “encourage” isn’t exactly accurate either.

At the 1/26 meeting and, according to the Stantons also at the October 26 meeting, Ms. Schaefer told those present that the insurance requirement is up to the lender. That is not altogether true, as shown in the excerpt below from the floodsmart.gov website:

Mandatory Requirements

Homes and businesses with mortgages from federally regulated or insured lenders in high-risk flood areas are required to have flood insurance. While flood insurance is not federally required if you live in a moderate-to-low risk flood area, it is still available and strongly recommended.

With respect to the above excerpt, it should be noted that banks are federally regulated and insured (FDIC), so the insurance requirement is not just for loans held by Fannie Mae and Freddie Mack. Only a home with a mortgage from an entity that has no links to the federal government is exempt, a relatively rare situation.

Linda Stefanick’s home is on Tullock Lake in Copperopolis. Like all the other homes on the lake, it was built at an elevation required by the County above the 515 foot mark. That is the height above sea level of the dam that creates the lake. Like the other properties, her parcel extends into the zone normally under water. Those properties were so drawn as to allow the owner to build a boat dock on the property.

There is some question as to whether Linda received notification from the County as to the flood status of her property. She does not recall it and cannot find it. She has also questioned everyone she knows on the lake. All of them say they did not receive the notice. The absence of those notifications was confirmed in a call to Susan Larson of Tri Dam, the agency that manages the dam and the lake. Her office received numerous calls from property owners who, like Linda, had not received notice from the County. Also confirmed by Ms. Larson was that fact that FEMA did not contact Tri Dam with respect to the properties that border the lake.

Notification issues aside, Linda learned of the flood-zone status of her property from the bank where she has her home loan (Chase). The bank began imposing a forced flood insurance policy on her in January, 2011 with premiums of $2,250 a year.

Since she didn’t know about the flood status until recently, she missed the chance at a do-it-yourself LOMA application. She has since been told she needs an application prepared by a certified engineer or surveyor with an estimated price tag of $2,000, where, it could be argued, the building permit itself is sufficient evidence that the structure is not in the flood zone. Easier yet would have been a call to Tri-Dam or the County.

Also on the subject of LOMA’s, as valuable as that document is to the property owner, it does not exempt the owner from flood regulations. In 2008, the Calaveras County Board of Supervisors approved ordinance 2955 rewriting chapter 15.06 of the County’s code dealing with flood prevention. If any part one’s property is in a flood zone, this 21-page ordinance kicks in. If you have an RV, for instance, you would be interested in the following excerpt:

Better get that RV running, licensed and insured, because it is otherwise not “ready for highway use.” Failing to do so, indeed with any violation of the ordinance, there is a price to pay.

Finally, lest you believe there is any wiggle room in your favor, the following clause is offered to set you straight.

Earlier, I mentioned FEMA’s fallback position to the failed assertion that the Calaveras River was the source of flooding on the Stanton’s property. That fallback position is that rainfall on the sloping land itself would produce the flooding – never mind that it has never happened according to the rainfall data available for over 100 years, data presented to Ms. Schaefer at the 1/26/11 meeting.

At the heart of FEMA’s flood map, and indeed at the heart of its strategy, is a definition of “flood” that seems to have been written with no thought to what a flood actually is, contributing to the notion that it was drawn primarily to ensnare millions of property owners in an insurance scheme.

FEMA defines a flood zone as one where there is a one percent chance of water rising to a level of one foot. Otherwise stated, water is predicted to rise to a level of a foot sometime over a 100-year period. Does the definition include any provision for damage created by the predicted rise in water? No. This could simply be a low spot on a piece of property that fills up when it rains hard, then drains off immediately afterwards with no harm done.

Another basic flaw in FEMA’s flood definition can be illustrated with the graphic below.

Drainage basin A has a steeply sloped groove so that the water may achieve a depth of one foot with relatively little flow. This topography is similar to that on the Stantons’ property. Basin A represents either a natural topography where the water has cut the groove, or a manmade ditch to contain and control the water, but would nevertheless be categorized as a flood zone by FEMA. In effect, a water containment structure, which would normally be considered worthwhile and which engineers design into a property for the very purpose of controlling runoff water, actually works against the property owner.

Drainage basin B is a relatively shallow structure that does not contain the water, but allows it to flow uncontrolled. Since it would not achieve the one foot depth with the same volume of water as in A, it would not fall within FEMA’s definition.

Containment topography or not, in the Stanton’s case, even the worst storm in 10 years didn’t cause a rise in water in that gully to a level of a foot, but in a 100 years, who knows? If it did, would it cause any damage? No. Would it result in flooding downstream, somewhere in the flat country? Perhaps, but certainly not at the higher elevations. That said, the 100+ year rainfall data the Stantons presented Ms. Schaefer showed the only recorded flooding over that period of time was in 2006, occurring along Cosgrove Creek near La Contenta, a well-known problem spot hereabouts.

The issue of man-made and professionally engineered runoff containment ditches having no positive effect, and possibly a negative effect on a piece of property (as far as FEMA is concerned) is precisely the prospect facing Tom Coe and his 650 acre industrial parcel near Valley Springs.

In the 60’s the site included a clay mining operation engineered (including water runoff features) by the engineering and construction giant Bechtel Corp. The plant site is still there and operating with a variety of light industrial enterprises, but Coe’s plans for the parcel include a community college campus, medical facility and industrial sites with links between education and industry - a truly visionary project that would be the jewel of the County.

As difficult as it will be for Coe to see his vision realized under normal circumstances, that picture has now been further blurred by a flood zone designation placed on the property in spite of, or due to the very drainage ditch Bechtel engineered 50 years ago to divert ground water runoff around the clay mining operation.

The photo above is of the engineered drainage ditch taken on March 22, 2011, the day after several consecutive days of heavy rainfall. As can be easily seen, the ditch is more than adequate to the task. For comparison purposes, the photo below taken on the same day, of Cosgrove Creek at the Gold Creek community a couple of miles downstream past Valley Springs shows the creek quite full, but not overflowing.

Referring to the previous photo of the drainage ditch - if the definition of a flooded waterway is one that, at a minimum, includes the fact of its banks overflowing, in order for the Coe property to experience flood conditions emanating from that ditch, the lower elevation valley in the background of that photo, land that includes Cosgrove Creek, would have to be approximately 20 feet under water. As shown previously, however, that is not how FEMA defines a flood.

Both the Stanton and Coe examples sound similar to a situation in Kansas which led to a lawsuit against FEMA as reported by msnbc.com in January of 2010, just one of many examples of communities trying to fight back against FEMA.

FEMA sued

Garden City, Kan., has sued to prevent FEMA's proposed map for the city from taking effect. The map for the first time designates areas around two decades-old drainage ditches as flood prone, even though the ditches have never been a problem, said Kaleb Kentner, the city's community development director.

To a point, FEMA knows it needs the cooperation of the County to further its agenda. Indeed, at another public meeting limited to real estate brokers and insurance agents on October 26, 2010, NFIP representative Jana Critchfield told her audience that the County was part of its “Cooperating Partners Program,” and for that participation was to get a percentage of the insurance premiums. Calls to the County Auditor’s office to confirm that information, at this writing (over three weeks later), have not been returned. Again, the carrot is offered, in this case to the County, but there is also a stick. At the end of the day FEMA can tell the County to pound sand.

At the January meeting, Ms. Schaefer informed us that the County can reject FEMA’s flood map, but doing so would disqualify all property owners in the County from obtaining flood insurance. Remember, FEMA/NFIP is the only domestic underwriter of flood insurance.

All is not lost, however, because according to Ms. Schaefer, those property owners could obtain flood insurance from an overseas insurer, Lloyds of London, that is if they can afford the $4,000 price tag.

Currently, the entire county is in a FEMA “re-study,” meaning FEMA is to reconsider the flood zone map of the County it previously drew. They will do so considering new data to be gathered by planes overflying the County with instruments that are capable of creating much more detailed topographical data than is currently available.

The existence of the re-study itself raises an interesting question. Why is anyone in the County being hit with insurance bills if FEMA is reconsidering its flood map? Further, is the survey data the issue, or is it FEMA’s definition of a flood? That definition is not a data issue; it is an issue involving logic, reason, reality and practicality.

FEMA inserted itself into the flood map business in our county in 2007. At that time, there were 2200 parcels that included some flood zone. FEMA’s flood definition and engineering added 5070 parcels into flood zones. It more than tripled the total number of parcels to 7270. That’s in a county with 43,370 total parcels and a county that is dominated, not be flat land and large rivers, but by hills, has nearly 17% of its parcels in a flood zone. How is that possible?

Where has the county, and the state for that matter (the Department of Water Resources draws flood maps for the state), been all these decades? Has their engineering and local knowledge been totally lacking, or is that they knew a flood when they saw one?

The County has an obligation to protect its citizens against federal schemes like this one which appears to be nothing more than taxation through regulation and a blatant attempt to get millions of no-risk property owners to subsidize the insurance pool for the benefit of those in high-risk areas, most of which are thousands of miles from here.

By comparison, consider that the U.S. Justice Department has been investigating and prosecuting perpetrators in the sub-prime home loan scandal. Among the allegations are that lenders falsified loan applicants’ information, and employed other fraudulent tactics resulting in loans being granted to unqualified borrowers leading lenders profiting from a bad loan that they quickly sold on the securities market, or to the Feds.

We know the result of the sub-prime home loan meltdown, but I question how different is the behavior of FEMA? Has it falsified information on the flood status of properties in an attempt to force owners to buy flood insurance? Has it placed properties in flood zones without sufficient evidence? Has it pressured, scared or fooled owners into buying flood insurance who either did not need it, or before there was sufficient evidence of the need? Has it ignored historic rainfall and flood data in drawing its maps? Has it concocted a definition of flood solely for the purpose of expanding its own pool of insurance policy holders?

The evidence shows that “all of the above” would be the accurate answer; or at the very least that FEMA has been so wanton in its behavior as to produce the same result. Finally, isn’t FEMA’s take-it-or-else position with the County akin to putting a gun to the head of the County at the expense of thousands of property owners (and how many nationwide)?

FEMA is an insurance monopoly with tremendous power. It is being allowed to do five things that any unscrupulous monopoly power would love to be able to do and, if they did, might well face prosecution for doing so; 1) It is being allowed to invent the need for its product (insurance), 2) It is being allowed to mandate the purchase of its product, a product only it sells, 3) It controls the price of its product, 4) It is being allowed to employ, coerce, or bribe (pick your favorite verb) other government entities (counties) to assist it, and 5) It is being allowed to deny the purchase of its product to anyone who lives in a county that won’t play ball, thereby forcing the county to hand over thousands of new policy holders to FEMA or cause those who actually need the insurance to lose that coverage.

Consider a scenario whereby the actions of FEMA were being undertaken by a private, for-profit insurance company, one that had a similar monopoly. Wouldn’t that company be subjected to the same criticisms and even outrage we have seen from the state and federal government over the actions of for-profit health insurance companies, for example? Where is that outrage and government intervention when the perpetrator is a government insurance entity? Where is the call for intervention? Where is the call for an investigation, or is this a case of the fox being in charge of the hen house?

Consider the long-term effect of a flood zone designation on a piece of property. It is a black mark on that property forever, lowering its value. Those lower values relate directly to property taxes collected by the County and thus the revenues to the County. With respect to properties zoned for commercial or industrial use, that black mark can turn them into useless parcels on which no finance company will back a project.

Finally, consider the effect on property owners who are struggling to hold on to their homes, where many others have lost them due to foreclosure. What will happen to those property owners who are on the edge of foreclosure and who will now see expensive new premiums added to their mortgages? How many more people will lose their homes - homes that will go into foreclosure, will be resold at a lower cost, resulting in even lower levels of property tax revenues, setting aside the devastating effects of that loss on the families?

I call upon the Board of Supervisors to do the following:

1. Call public hearings specifically to hear more examples of property owner experiences in dealing with FEMA. That hearing would record examples of the pressure FEMA put on property owners to buy insurance now, at the cheaper price, rather than take the risk associated with delaying purchase until more facts could be gathered. The County would hear that FEMA did not appear interested in answering questions about its findings or how to appeal them, but focused on the “buy it now” scenario, using scare tactics to advance its agenda.

2. I call upon the County to investigate the role our planning department has played in this process. To what extent has the department, with all of its local knowledge, challenged FEMA, or to what extent has it become an extension of FEMA via the “Cooperating Partners Program?” Further, to what extent has FEMA tied the hands of the County with its take-it-or-leave-it powers?

3. I ask the County to reveal any and all incentives offered and/or received from FEMA either to the County as a whole or any of its departments.

4. Draft a resolution to be sent to Congressman Lundgren’s office calling for a realistic and practical definition of “flood” to govern FEMA’s flood maps. To make that definition practical and real, it should be based on real engineering and the predictability of significant monetary damage to the property. No harm, no flood. The existence of water on a property, even water a foot or more deep, does not a flood make.

5. The resolution should also ask Lundgren’s office to initiate an investigation into the practices of FEMA and to suspend all actions based on FEMA’s new flood maps nationwide, including mandated insurance, until such an investigation is complete. Hopefully, that investigation will lead to Congressional hearings.

6. The resolution should further ask the Congressman’s office to investigate the relationship between FEMA and its subcontractors, including Michael Baker Engineering and to determine whether the authority held by the subcontractors is appropriate.

7. I ask the board to call upon the state’s Insurance Commissioner to also investigate the actions of FEMA, just as it would a private insurance company.

8. As an interim measure, the resolution should call for re-establishing the do-it-yourself LOMA application process and extending the deadline for that process through 2011. There is sufficient evidence to suggest that the County may not have notified everyone who was newly placed in a flood zone. That should be looked into, as it denied them a shot at a do-it-yourself LOMA. More significantly, it took FEMA years to develop their flood map and they admit they still don’t have it right. Forcing property owners to disprove the most important part of it, and in only a few weeks, was unreasonable and forcing them to spend considerable money to do likewise is also unreasonable.

I also call upon all property owners affected by this fraud to take action. When you made the deal to buy your property, probably the largest financial deal of your life, you made it based on the property information you were given, including the flood status determined by the County. If that property was not in a flood zone, you paid a premium for that status. Now FEMA, with or without the aid of the County, is retro-actively changing the deal you made without a quid pro quo.

If the County isn’t able to affect an end to this insurance fraud, I recommend you immediately request a re-assessment of your property values for tax purposes. The government can’t have it both ways. If it is going to devalue your property, there must be a quid pro quo. If property owners want their government to act in their best interests, the best way to do so is to act against the government’s primary interest, which, unfortunately, appears to be money.

|